By Brent A. Gloy

With commodity prices tumbling one of the key supports for sky high farmland values is changing rapidly. As economic returns in the farm sector fall, we should expect that the other key driver of high farmland prices, low interest rates, will come into much greater focus. Even with elevated profitability of recent years, capitalization rates on farmland have steadily drifted lower, meaning that the ratio of current income to farmland prices has fallen. In other words, farmland prices have grown more rapidly than current income. While this has made sense in a growing income and falling interest rate environment, this trend may be approaching its limit.

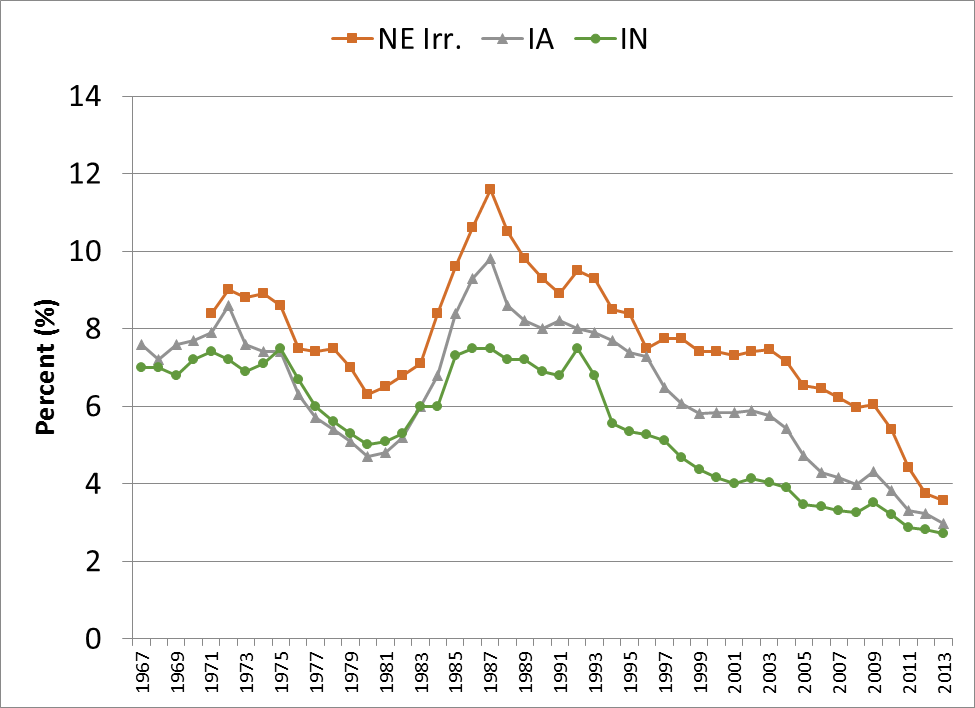

The capitalization rate on farmland is frequently expressed as the ratio of cash rent to farmland prices. The downward trend in capitalization rates for farmland can easily be seen in Figure 1 which shows the capitalization rates for Indiana, Iowa, and Nebraska irrigated farmland. Starting in about 1987 capitalization rates have steadily trended lower. Today, they are at some of the lowest rates that we can find in historical data. (Those interested in more details on the relationship between capitalization rates on farmland and ownership returns may find a recent study by my colleagues interesting).

Figure 1. Capitalization Rates for Nebraska Irrigated, Iowa, and Indiana Farmland, 1967-2013. Sources: Data were compiled various land value and cash rent summary reports published by the National Agricultural Statistics Service.

I have argued many times (here and here for example) that this trend either means that 1) people expect income to grow rapidly in the future and/or 2) that people expect interest rates and capitalization rates to remain low for the foreseeable future. Until recently, both looked like reasonable bets. As profitability has fallen it means that, other things equal, rates must remain low to keep farmland prices high. In other words, if incomes fall people must be willing to pay an even higher price for current farmland earnings.

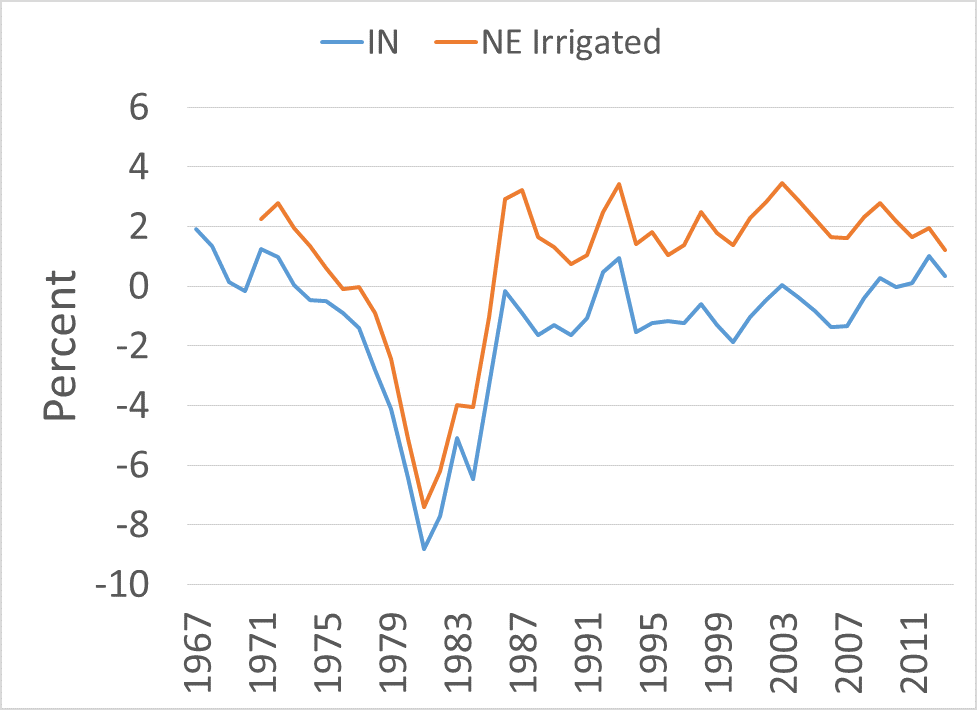

Today’s very low capitalization rates might be cause for concern if it were not for the fact that interest rates are also very low. This is most easily seen in Figure 2 which is a graph of the spread between the yield on 10 year US Treasury bonds and the Indiana and Nebraska Irrigated farmland capitalization rates. Negative numbers mean that the capitalization rate is lower than the 10 year bond, and positive numbers indicate that the capitalization rate is higher. You can see that the spread for both states is small, but by no means unusually small.

These spreads indicate that people are willing to accept a rate of return on farmland that is lower to slightly higher than the return on the 10 year Treasury Bond when purchasing farmland. There are several reasons why this might be the case. Farmland returns typically grow over time so the underlying asset usually appreciates. In other words, some of the return to farmland comes from income and some from expected capital gains. Treasury Bonds do not appreciate and will only ever pay holders the face amount of the bond.

Except for the farm crisis period of the 1980s, Indiana farmland has typically traded at 0 or up to 200 basis points less than 10 year Treasury Bonds, while Nebraska irrigated has traded 150 to 300 basis points above 10 year Treasury Bonds. Irrigated farmland would typically earn a higher current rate of return because it requires investment in depreciable equipment as well as a depleting resource (groundwater).

The notable exception to these ranges is the late 1970’s and early 1980’s. During the beginning of that period farmland prices were rising much faster than farm incomes. Then interest rates rose rapidly AND farm incomes and cash rents fell. This caused the spread to become very negative. In the 1980’s values couldn’t fall fast enough to bring the spread back into a reasonable range and the spread initially became very negative. Of course this situation eventually changed as land values fell dramatically and capitalization rates returned to a more typical level.

Figure 2. Farmland Capitalization Rates Less 10 Year U.S. Treasury Yields, 1967-2013.

So what does all this mean in the context of our current situation? When you look at the spreads between farmland and the 10 year bond, the current low capitalization rates on farmland make more sense. The capitalization rate is low because interest rates are low. Given that the Federal Reserve is now beginning to signal that short-term interest rates may rise in the next couple of years, one must ask the question of what would happen if interest rates were to increase?

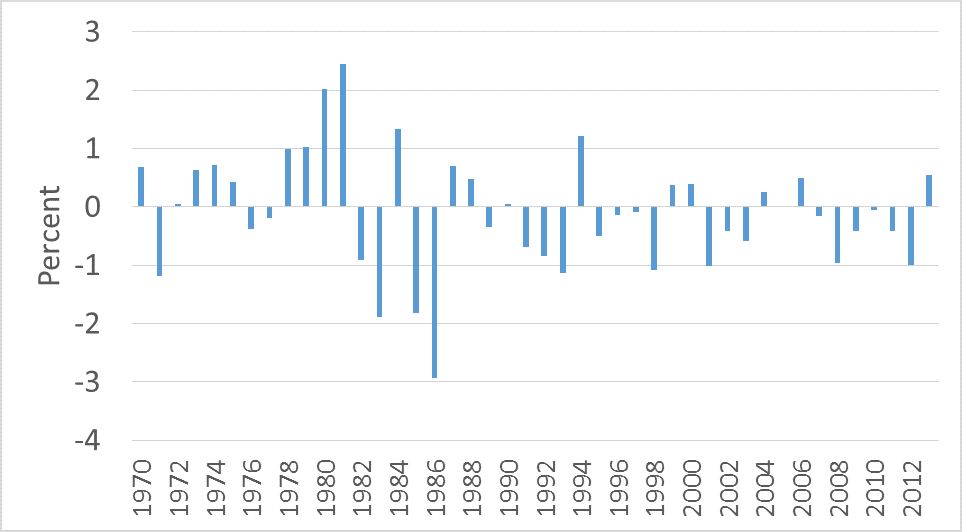

Figure 3 shows the annual change in 10 year Treasury Bond rates since 1970, in percentages. A value of 1 means that the rate increased by 100 basis points over the course of a year. You can see that only on a few occasions have 10 year rates risen by more than 100 basis points in a year. However, when they do, the spread between the treasury bonds and farmland tends to initially shrink or become more negative. In my opinion this is largely due to the fact that cash rents and land prices are slow to adjust (see this post for more on that topic).

Figure 3. Annual Changes in the Yield on 10 Year U.S. Treasury Bonds, 1970-2012.

In our current situation it is also clear that were longer term interest rates to rise, in order for farmland prices to remain constant, capitalization rates would have to fall even further unless cash incomes were to rise (something that now seems unlikely). While capitalization rates might fall further relative to the 10 year Treasury in the short-term (as they did in the late 1970’s and early 1980s) it is somewhat unlikely that they would do this for several years.

Overall, with lower commodity prices and returns available to farmland, it becomes even more imperative that interest rates stay low to hold farmland values at current levels. It is also true that it is very difficult to forecast future interest rates and long-term rates may stay very low for the foreseeable future. While a perfect storm of higher farm profitability and low interest rates drove farmland prices much higher, we must now be on guard for the unwinding of this situation which will likely begin to pressure farmland prices.