By Brent A. Gloy

Farmland values should reflect the expected present value of the future earnings that the farm might generate. This sounds nice in theory, but requires that one make forecasts of the present value of future farmland earnings, something that is inherently difficult to do well. Understanding how people think about this has been something of an obsession for me. We have asked many different people questions about their estimates of farmland values and forecasts of future earnings and have been surprised to find the lack of a strong positive relationship between these variables.

Recently, the USDA long-range commodity price baseline projections caught my eye. I generally pay little attention to the baseline as it is not really meant to be a forecasts of the future, but rather what the future might look like if today’s conditions persist over the next 10 years. However, I also realize that in order to come up with an estimate of the expected value of future earnings we must be able to say something about future prices, yields, and costs, all of which the USDA considers, so we decided to give them a second look.

We wondered how their view of the future has evolved over time. Could we learn something from these efforts and take away anything that helps us to better understand farmland values? In the coming posts I examine these projections and will eventually use them in some hypothetical calculations for the case of Indiana farmland values.

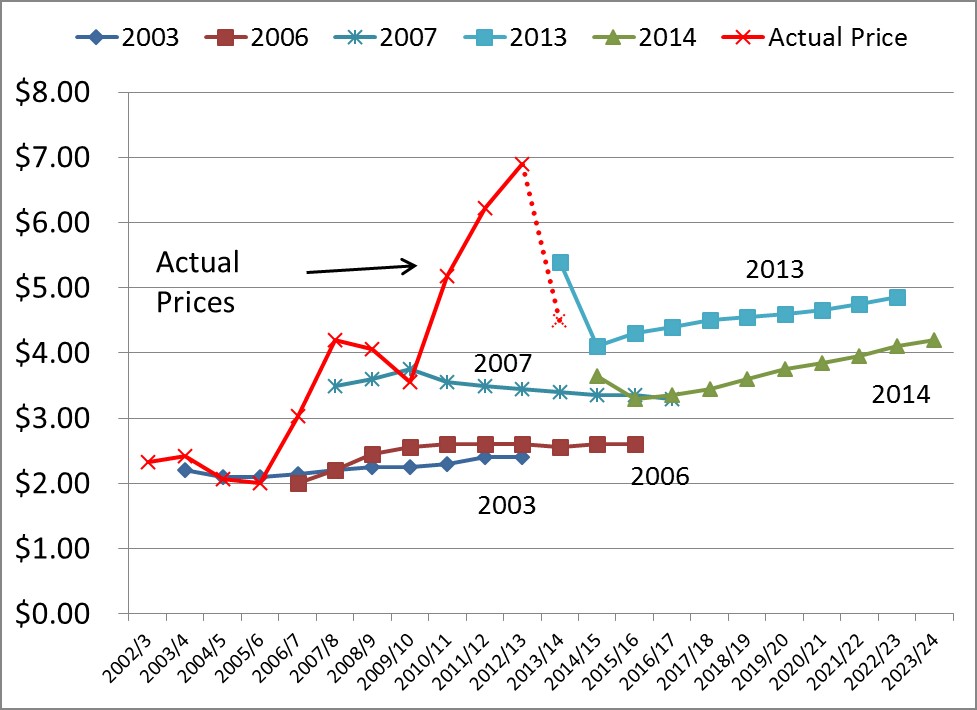

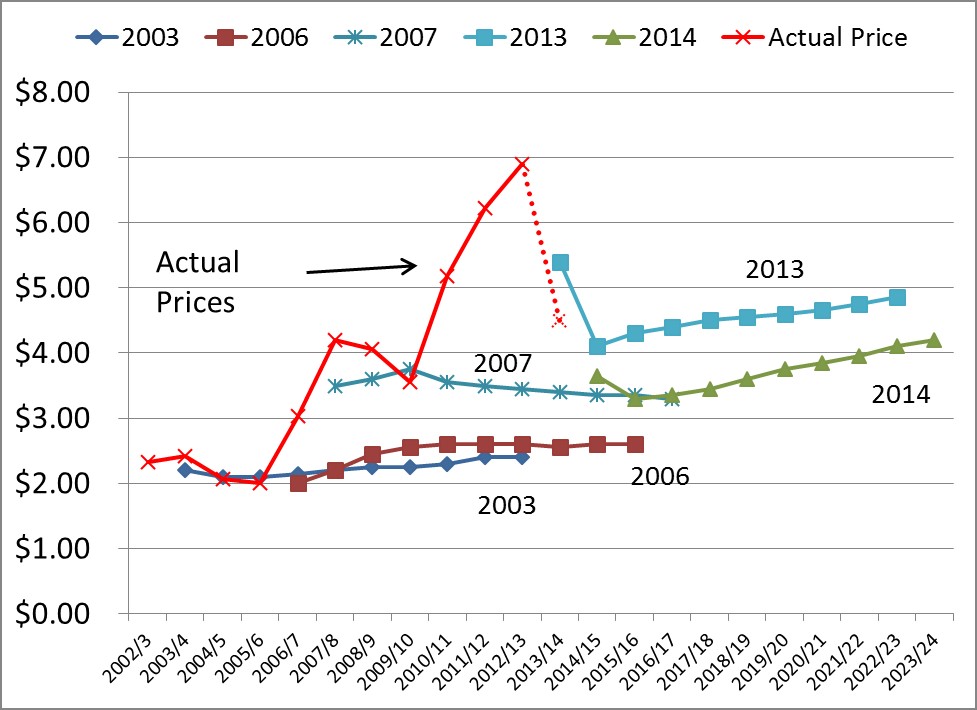

The USDA baseline corn prices are shown in Figure 1. A line represents the forecast made at the beginning of various years starting in 2003. For example, the 2003 line runs from the 2003/4 to 2012/13 marketing years. The actual marketing year prices are also shown on the graph. You will note that the realized prices have been consistently higher than the forecasts made by the USDA and in many cases substantially so.

There are several things that one might take from this chart. First, one can see how the projected prices for any given year have evolved over time and that these changes can be dramatic. For instance, in 2003 the USDA had projected the 2011/12 price at $2.40 per bushel. By 2006 this forecast the price projection was increased to $2.60 per bushel. Then, in 2007 a large increase occurred when the projection was increased a whopping 35% to $3.50 per bu. By 2011 the forecast for the 2011/12 crop year stood at $4.80, double the value released in 2003.

For farmland with 200 bushel per acre capacity the difference from the initial forecast to the final forecast would represent a revenue difference of $480 per acre! This highlights the great difficulty that has been associated with long-term forecasts in a rapidly shifting supply/demand environment and helps explain the dramatic increases seen in farmland values.

Second, one can see that in many years since 2006/07 the actual prices that were received exceeded those that the USDA had forecast at any point in time. The lone exception to this was the 2009/10 crop year when the actual price received was $3.55 per bu. This indicates that USDA has been somewhat skeptical that the price levels that have been achieved in recent years are likely to be sustained. In fact, since 2009 the forecasts have all shown USDA’s belief that prices will moderate to lower levels and then trend upward slightly. This is most easily seen in the 2013 forecast which shows a substantial drop (32%) occurring from 2013/14 to 2014/15 and then prices steadily increasing back to $4.85 per bu by 2022/23.

The most recent projection follows a similar pattern to the 2013 projection with an initial decline followed by a slight improvement over time. However, the prices in the 2014 forecast are substantially below those in the 2013 projection. The average over the 10 years of the 2013 projection was $4.61 per bushel and the average of the 10 years in the 2014 projection is $3.72 a 19% decline.

Figure 1. USDA 10-Year Corn Price Forecasts, Various Years 2003-2014a.

Figure 1. USDA 10-Year Corn Price Forecasts, Various Years 2003-2014a.

a The forecasts are for the 10 years beginning with the crop to be planted in the forecast year, e.g., the 2003 forecast included the 2003/4 to 2012/13 marketing years.

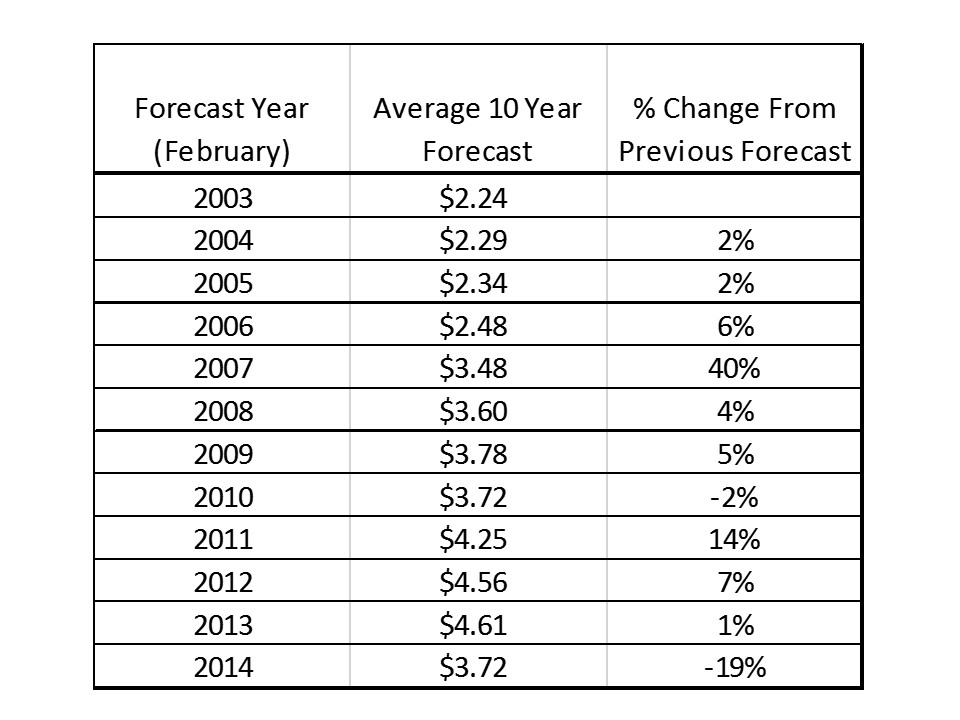

Another way to look at the shifting price expectations in the baseline is to average all ten years of the projection. Table 1 shows the average of the 10 year baseline projections for each forecast date. Starting from a value of $2.24 per bu. in 2003 the average of the 10 year forecasts increased modestly until 2007 when they jumped 40%, from $2.48 to $3.48 per bu. This increased view of the expected price of corn is a large reason why farmland values have exploded to the upside. Since 2007, the expected forecast prices have generally increased with another large jump of 14% occurring in 2011 and stand at $4.61 per bu. in 2013.

Table 1. Average USDA Long Term (10 Year) Corn Price Forecasts, $’s per Bushel, 2003 to 2013a.

a The forecasts are for the 10 years beginning with the crop to be planted in the forecast year, e.g., the 2003 forecast included the projections for 2003/4 to 2012/13 marketing years.

a The forecasts are for the 10 years beginning with the crop to be planted in the forecast year, e.g., the 2003 forecast included the projections for 2003/4 to 2012/13 marketing years.

The table is also useful for illustrating how difficult it is to forecast commodity prices 10 years into the future. From 2003/4 to 2011/12 the average price received was $3.64 per bushel, while USDA had forecast the 10 year average price from 2003/04 onward at $2.24 per bushel. While it is easy to say that these forecasts were obviously too bearish, it is important to point out that from 2003/4 to 2005/6 the forecasts looked optimistic as prices received over that time period averaged $2.16 per bushel. However, from 2006/07 to 2011/12 the average rose to $4.38 per bushel as biofuel demand, rapid expansion of export markets, and short crops tightened supply and demand. It is clearly very difficult to anticipate structural shifts that alter supply and demand.

The bottom line is that it can be very difficult to forecast commodity prices over such a long time horizon. The difference between beliefs of lower commodity prices and the higher prices that occurred is a large part of the reason that farmland values have increased so dramatically. In coming posts we’ll examine how yield and cost of production expectations have evolved over time. Then we will examine how one might use these expectations to examine the current situation in the farmland market and how sensitive the market might be to lower commodity prices and returns.