by David Widmar and Brent Gloy

When you think of March, two big events come to mind: the NCAA’s March Madness and the USDA’s Planting Intentions report. In both cases, speculation and anticipation is in full force on how the brackets and balance sheets will sort out. Furthermore, both the NCAA tournament and U.S. spring crop plantings will likely have a few surprises.

This week’s post takes a look at the latest crop insurance and commodity price data to provide some insights on what 2017 planting might have in store.

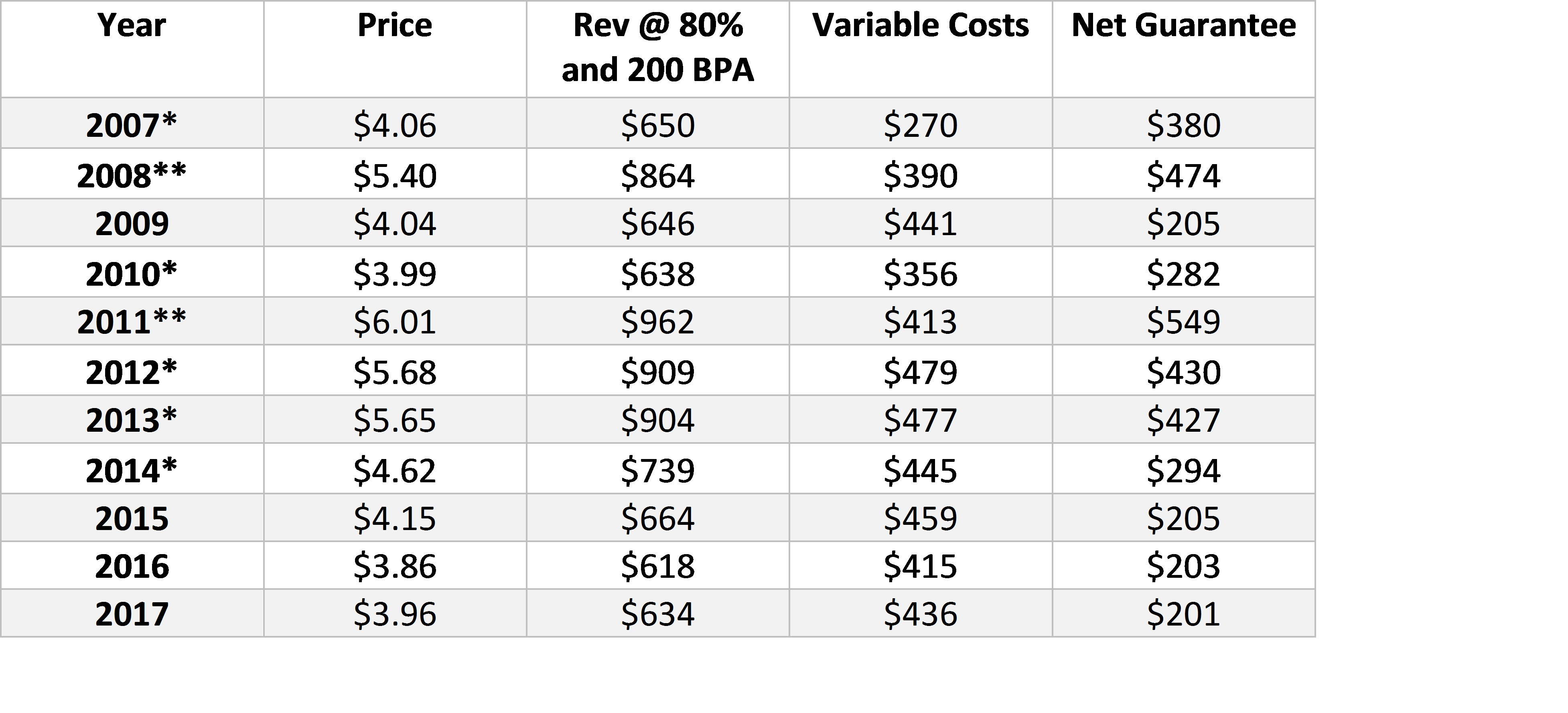

Corn Crop Insurance Guarantees

The crop insurance guarantee prices are set in February. For 2017, the corn price guarantee is $3.96 per bushel. This is $.10 per bushel higher than 2016, but the second lowest price of the past 11 years. Assuming a 200 bushel per acre insurance APH and 80% coverage, the crop insurance revenue guarantee is $634 in 2017 (Table 1).

The table also shows Purdue’s budgeted variable costs in the fourth column and the net that remains after subtracting the variable costs from guaranteed revenues. The net guarantee for corn has remained flat for the last three years. Despite falling variable costs, the 2017 net guarantee is the lowest seen in the last 10 years.

Table 1. Corn Crop Insurance Guarantees for an Indiana Farm with 200 Bushel per Acre APH, 2007- 2017. * Indicates year where net guarantee was sufficient to cover 2017 estimated cash rent of $244 per acre.

* Indicates year where net guarantee was sufficient to cover 2017 estimated cash rent of $244 per acre.

** Indicates year where new guarantee was sufficient to cover all 2017 fixed costs ($445).

Similar calculations for soybeans are shown in Table 2. Here, one can see that the revenue guarantee for soybeans is considerably ($65 per acre) higher in 2017 than 2016. While variable cost increases have eaten away at some of the gain, the net revenue guarantee for soybeans has increased $36 per acre over 2016. Unlike corn, the net guarantee is higher than at any time in the last three years and exceeds the corn net by $47 per acre. This is one reason that many people expect soybean acres to increase.

Still, it is important to realize that the data in Tables 1 and 2 represent an approximation to conditions in Indiana. One should keep in mind that costs, yields, and farm level prices will vary considerably throughout the country. As we pointed out in an earlier post, these differences can be significant and lead to different conclusions for different situations. Still, for a farm with a similar situation as depicted in these tables one would think that soybeans would be very, very competitive with corn.

Table 2. Soybean Crop Insurance Guarantees for an Indiana Farm with 60 Bushel per Acre APH, 2007- 2017.

* Indicates year where net guarantee was sufficient to cover 2017 estimated cash rent of $244 per acre.

* Indicates year where net guarantee was sufficient to cover 2017 estimated cash rent of $244 per acre.

** Indicates year where new guarantee was sufficient to cover all 2017 fixed costs ($445).

Price Relationship

Another way to assess the relative attractiveness is to construct the ratio of soybean to corn prices. This ratio is shown in Figure 1. In it we graph the ratio of the crop insurance prices as well as those found in the Purdue crop budgets. As one can see, the current soybean to corn crop insurance price ratio is at its highest level over the period of 2007 to 2017. This is just more evidence of the relative attractiveness of soybeans versus corn. However, one should keep in mind that recent analysis by Todd Hubbs and Darrel Good at FarmDoc Daily who noted that this ratio has somewhat limited ability to predict acreage shifts among the crops.

Figure 1. Soybean to Corn Price Ratios, 2000- 2017. Purdue Crop Budget and Crop Insurance Prices.

Figure 1. Soybean to Corn Price Ratios, 2000- 2017. Purdue Crop Budget and Crop Insurance Prices.

Thinking About Corn and Soybean Acres

While we (Brent and David) often speculate about the number of corn and soybean acres among ourselves, we don’t make a formal forecast – there are just too many ways to be wrong. With that said, we will provide a few thoughts on how things might shake out.

Figure 2 provides several insights for 2017 planting. While we generally dislike dual-axis graphs, we will make an exception here. The graph shows total corn and soybean acres on the left axis and the percent of that total planted to soybeans on the right axis. There are a couple of things that we can discern from this graph. First, total corn and soybean acres (graphed in blue) have increased considerably over time. In fact, at 177 million acres in 2016, total corn and soybean acres were at a 27-year high. This total acreage can be thought of as the total acreage pie that these two crops will split.

Looking to 2017 it’s completely possible to set another high for combined corn and soybean acreage. In other words, it seems plausible that the pie will continue to expand. Why? The USDA estimated in January that U.S. winter wheat acres were set to decline by 3.75 million acres in 2017. It seems likely many of these acres will migrate to corn and soybeans.

The second data series graphed in Figure 2 is the share of total corn/soybean acres planted to soybeans (graphed in orange). This is analogous to the size of the two slices of the pie. Historically, soybean acres have been less than 50% of total corn/soybean acres. The share was as high as 49.5% (2001) and as low as 40.9% (2007). Over the 27 years, the soybean share has averaged 46.3%. Even though the share was lower in 2016 (47.0%), it was still above average.

Perhaps most noteworthy is the frequency at with the soybean share has been 48%. A total of 6 times (or 22% of the time) the soybean share of total corn/soybean acres has been 48.0%-48.9%. While these small changes in share at first seem insignificant, it is important to realize that at the 2016 planting levels each 1% amounts to 1.7 million acres.

Figure 2. Total U.S. Corn and Soybean Acres and Share of these Acres Planted to Soybeans, 1990 – 2017.

Figure 2. Total U.S. Corn and Soybean Acres and Share of these Acres Planted to Soybeans, 1990 – 2017.

Let’s Look at a Few Scenarios

Considering the two measures in figure 2 – total corn/soybean acres and the share of soybean acres – a few key insights can be made by considering different scenarios around these metrics. Let’s first think about total corn and soybean acres (the size of the pie) and then the proportion of the pie that goes to each crop (the size of the two slices).

With respect to the total corn/soybean acreage we will look at two possible scenarios. First, we consider a large increase in total corn/soybean acres. Even though total corn/soybean acres were at a 27-year high of 177 million acres in 2016, an increase is again likely in 2017. In fact, this could be up as much as 3.75 million acres if all the reduction in winter wheat acres is planted to corn or soybeans. This assumption ignores changes in spring wheat acres and cotton. Cotton acres may be higher in 2017 given strong prices. This assumption also ignores changes in small acreage crop and hay. In short, this is an aggressive assumption about acreage expansion. Second, we will look at the situation where combined corn/soybean acreage is unchanged from 2016.

Now consider the share of total corn/soybean acres devoted to soybeans. Here again, we look at two scenarios. Given the crop insurance and price signals, an increase in this share seems possible. One scenario is a modest shift toward soybeans with 48% of total corn/soybean acres planted to soybean (compared to 47.0% in 2016). While this is an increase over 2016 it is slightly less than the share of acres devoted to soybeans in 2015 (48.4%). The second scenario is a planting rotation that strongly favors soybean (a soybean share at 49.5%). This share is a much more aggressive assumption toward soybeans and is a level last approached in 2006 (49.1%).

Given these assumptions and scenarios, four potential outcomes of 2017 planting of corn and soybean acres is shown in Table 3. Again, these are not estimates, but rather a range of outcomes given historic data.

The first important observation is that in all scenarios more soybeans are planted. The range of the soybean acres is 85.2 million to 89.7 million acres (up 1.8 million and 6.3 million from 2016). The most aggressive increase in soybean acres (up 6.3 million acres) would require a large increase in total corn/soybean acres and a simultaneous increase in the share of total acres captured by soybeans reaching historically high levels; a tall order!

In three of the four scenarios, corn acres are down. The exception is with a large increase in total corn/soybean acres and an acre share that only modestly favors soybeans. Here, corn acres would increase by 0.2 million acres over 2016 levels. In other words, if soybean’s share of acres reach 48%, it is difficult to find situations where corn acres would increase in 2017.

Table 3. Potential 2017 Corn Soybean Planting Scenarios.

Finally, given the ranges used in these scenarios, the share of soybean acres is of greater importance for determining final acreages. For example, assuming total acres are unchanged from 2017, an increase in the share of soybean acres (from 48.0% to 49.5%) brings about an additional 2.6 million soybean acres. On the other hand, given a share that strongly favors soybeans (49.5%) and increasing total acres by 3.75 million, brings in an additional 1.9 million soybean acres.

The magnitude of these changes are based on the assumptions we made, but these are ranges that we feel are possible and reasonable.

Final Thoughts

A couple of things are important in thinking about corn and soybean acreages. We have framed the discussion around 1) the total number of acres devoted to these crops and 2) the distribution of acres between the two. Of these two, the distribution may deserve the most attention. It has varied considerably in recent years and if it returns to a level of 2015 will result in significantly more soybean acres in 2017. The total acres are also key and here the debate seems to be focused on how many acres will be gained at the expense of wheat and perhaps lost to cotton and other crops.

Overall, the assumptions that we used in this post suggest that soybean acres will likely increase anywhere from a little to a lot. It would take scenarios outside what we have considered to result in decreased soybean acreage. However, that is not to say it can’t happen. Given our assumptions, corn acres declined in three of the four scenarios, but it would take a strong shift in the share of the crop going to beans to result in large declines in corn acreage. Again, it is not to say that either situation can’t occur.

It’s important to note the USDA’s March prospective plantings estimate is subject to a lot of changes. This is because a large number of factors impact planting decisions. The most obvious is weather. Previous yields and local economic situations are also key. However, one of the most tricky elements of predicting plantings is that market reactions to the estimate can influence decisions. In other words, a disconnect between the USDA’s estimate and the markets’ expectations will impact commodity prices. If changes in commodity prices are significant enough, it will begin to change producer decisions. In our post last year we used a quote by someone much wiser than us to summarize this idea and we think it is worth repeating:

“In some ways, predicting the economy is even more difficult than forecasting the weather, because the economy is not made up of molecules whose behavior is subject to the laws of physics, but rather of human beings who are themselves thinking about the future and whose behavior may be influenced by the forecasts that they or others make.”

Ben Bernanke –“Flexibility and Optimism in an Unpredictable World” Boston College Law Review. September 2009; pg. 942.

Interested in learning more? Follow the Agricultural Economic Insights’ Blog as we track and monitors these trends throughout the years. Also, follow AEI on Twitter and Facebook.

Photo Source: Flickr/USDA NRCS South Dakota